Why I switched to Xapo Bank 3 years ago

My initial problem was simple but frustrating to solve: I needed a personal USD account, separate from my US LLC business, without living in the United States. My LLC takes in USD and EUR through two rails — Wise Business (multi-currency account for US and European client wires) + Stripe (online card payments, payouts land in Wise Business) — but I wanted a clean personal account, USD-native, for owner draws without going through a French bank (FX fees + zero yield + accounting headache). Separating business from personal is crucial for tax and operational reasons.

I tested Wise — excellent for international transfers, but 0% yield on USD balances and technically not a bank (e-money license). I tested Revolut — handy for daily life but the USD side isn't a real routing-number account in most jurisdictions. Coinbase for Bitcoin — but it's not a bank, just an exchange, with no deposit protection.

One thing that pushed me to find a real licensed bank: Revolut froze my account without notice and locked my funds for several days, with no explanation. The compliance team took weeks to respond, and I had zero clear regulatory recourse. When your personal or business liquidity depends on a tool, that's unacceptable. This is the structural risk of e-money institutions like Revolut or Wise (which don't hold full banking status): no FDIC/FSCS-equivalent deposit protection, no clear resolution framework if you get locked out. With Xapo Bank (regulated by GFSC + Gibraltar Deposit Guarantee Scheme), you at least have a regulatory framework protecting you — and a supervisor (the GFSC) you can escalate to. This isn't a theoretical detail: it's the practical difference between "fintech" and "bank".

Xapo Bank ticked the four boxes the others were missing:

- Real banking license (Gibraltar FSC, Permission No. 23171) with Deposit Guarantee Scheme

- USD account with international routing number, usable to receive wires from anywhere

- Physical VISA card delivered to my international address, working in most countries

- Native Bitcoin custody under the same banking license, with yield (modest but real)

No other institution combined these four for my non-US/non-UK profile. I took the plunge in 2023 and haven't regretted it — with some caveats detailed below.

The product in 2026 — what you actually get

USD account with routing number

This is the core of the product for my use case. You get a real US routing number + account number that works for ACH and international wires. Concretely, my LLC sends owner draws (transfers to owner) from its Wise Business account to this Xapo personal USD account — everything stays in dollars, zero conversion loss. The 3.35% yield on personal USD balances sitting in the account is significantly higher than Wise (0%) or most neo-bank accounts.

Worldwide VISA card

A VISA Platinum card delivered to your address (Xapo ships to most countries — check their site for your specific jurisdiction). No foreign transaction fees, works anywhere VISA is accepted. I use it as a secondary payment method when traveling and for USD online purchases. Solid, no surprises.

Bitcoin custody under a banking license

Your BTC is held in bank-grade custody by Xapo using their legacy physical bunker infrastructure (a leftover from their pre-2019 institutional business, acquired by Coinbase). 100% reserve policy — no fractional reserves. You can buy, sell, and hold BTC in the same app. BTC yield of 0.50% (modest but with no smart contract risk).

Mobile app and UX

The app is sober, functional, no fluff. Doesn't have Revolut's glamour but it's clean. Push notifications on every transaction. Biometric authentication. Handles multiple accounts (USD, EUR for some plans, BTC) in the same interface. No navigation friction.

Yields — 3 BTC tiers, not just one

Yield isn't a single rate: Xapo exposes three distinct BTC yield products in the Savings & Investments tab, plus USD Savings and a Stocks & ETFs section.

- USD Savings: 3.35% APY — yield generated within the banking license framework, no DeFi smart contract exposure. For "comfortable" cash.

- BTC Credit Fund: 2.54% APY — a newer product (marked "New" in the app), significantly higher yield than the standard tier. Reserved for large stacks: minimum 2 BTC required (~$150,000 USD at current rates). If your BTC stack is below, you're capped at the next tier.

- BTC Savings: 0.5% APY — basic tier for smaller stacks, liquid BTC, no minimum.

- BTC Vault: 0% APY — maximum-security cold storage, no yield. For the portion of your stack you want to keep frozen.

You allocate your BTC balance across the three tiers in the app — for example 80% Vault + 20% Credit Fund for a security/yield mix.

Stocks & ETFs (integrated broker)

A feature few licensed banks offer: Xapo has an integrated stocks and ETF broker in the same app. You can buy SPY, VOO, money market ETFs, individual stocks directly from your USD account. Comparable to what Trade Republic or Revolut Stocks offers, but this time under a real banking license. For an expat who wants to consolidate banking + brokerage USD in one product, that's a solid plus.

Loans (instant collateral-backed loan)

You can borrow USD against your BTC collateral directly in the app. Same mechanics as Celsius offered before collapsing — except here it's within a licensed Gibraltar bank with bank-grade custody. If you want to use your BTC without selling it (no taxable event), it's an option worth knowing. Not for everyone, but useful in certain tax scenarios.

Universal Money Address (UMA) and multi-rail deposits

The "Add funds" tab exposes all rails: SWIFT, ACH, Wire for USD, auto-conversion from EUR/GBP, USDC and USDT (converted to USD), and more recently Universal Money Address (UMA) for crypto transfers via a simple email-style address. UMA is a recent standard few banks have — handy for receiving crypto-ecosystem payments without giving out a blockchain address.

What works well after 3 years

1. The regulation is solid and verifiable

The GFSC license number (Permission No. 23171) is public and verifiable on the Gibraltar Financial Services Commission website. It's not "crypto wrapper disguised as bank" — it's a real credit institution with capital requirements, examination authority, and consumer protection obligations. The Gibraltar Deposit Guarantee Scheme covers your fiat funds like an FDIC-equivalent.

2. USD transfers are fast and reliable

Transfers from Xapo to other USD accounts generally take a few minutes for internal (other Xapo clients), and 1-3 days for external ACH. For someone used to European SEPA which clears in hours, it's the same league. Far better than classic international SWIFT delays (3-5 days for clients paying from the Eurozone).

3. Real multi-currency: EUR and GBP for my European clients

Killer feature for my profile working with a European client base. The "Add funds" tab exposes deposit rails in EUR (SEPA) and GBP, and withdrawals work both ways. When a French or German client pays me in euros, I can receive directly on Xapo — no European intermediary bank needed. Note: EUR and GBP are automatically converted to USD on deposit (the account is USD-centric), so you need to be OK with immediate conversion. If you want to keep EUR as your main currency, Wise or Revolut are better fits. If you want to consolidate in USD while accepting EUR/GBP client rails, this is exactly what you need.

4. The VISA card really works everywhere

Tested in multiple countries over these 3 years (Eurozone, Southeast Asia, Latin America). Accepted everywhere without surprise. No hidden FX fees. No manual verification requests for foreign purchases like some French cards do. A small detail that matters when you're traveling.

5. The 100% BTC reserve policy is reassuring post-FTX

The FTX collapse in 2022 highlighted the risk of fractional reserves in crypto. Xapo Bank has a structurally different model — your BTC is held 1:1, verifiable by audit. It's not self-custody (you trust Xapo with the keys), but it's noticeably safer than the average exchange that's defaulted over recent years.

6. Real private banking service: dedicated advisor + in-app calls

Support isn't just "decent" — it's a real private banking experience, which is rare at this price point. Every client gets a dedicated advisor assigned, reachable through the app to book a call. The in-app chat responds in minutes for standard questions (not hours like most neo-banks). Over 3 years, all my interactions resolved on first touch — with a real person who knew my file, not a chatbot or scripted T1 agent. Light-years from the frustrating standard of traditional banks where opening a ticket for an address change takes 3 weeks. For $1,000/year, you expect better than a chatbot — and Xapo delivers.

7. KYC is surprisingly fast for a real bank

Contrary to what many reviews say (often based on early 2021-2022 user experiences), Xapo Bank's KYC in 2026 is short and easy. Passport + proof of address + biometric selfie → typically a few days to approval in most cases. Faster than the official docs suggest ("3 days to 2 weeks"), and significantly faster than many traditional banks where opening an account can take weeks even for a resident. For a real licensed bank, it's an excellent speed/rigor tradeoff.

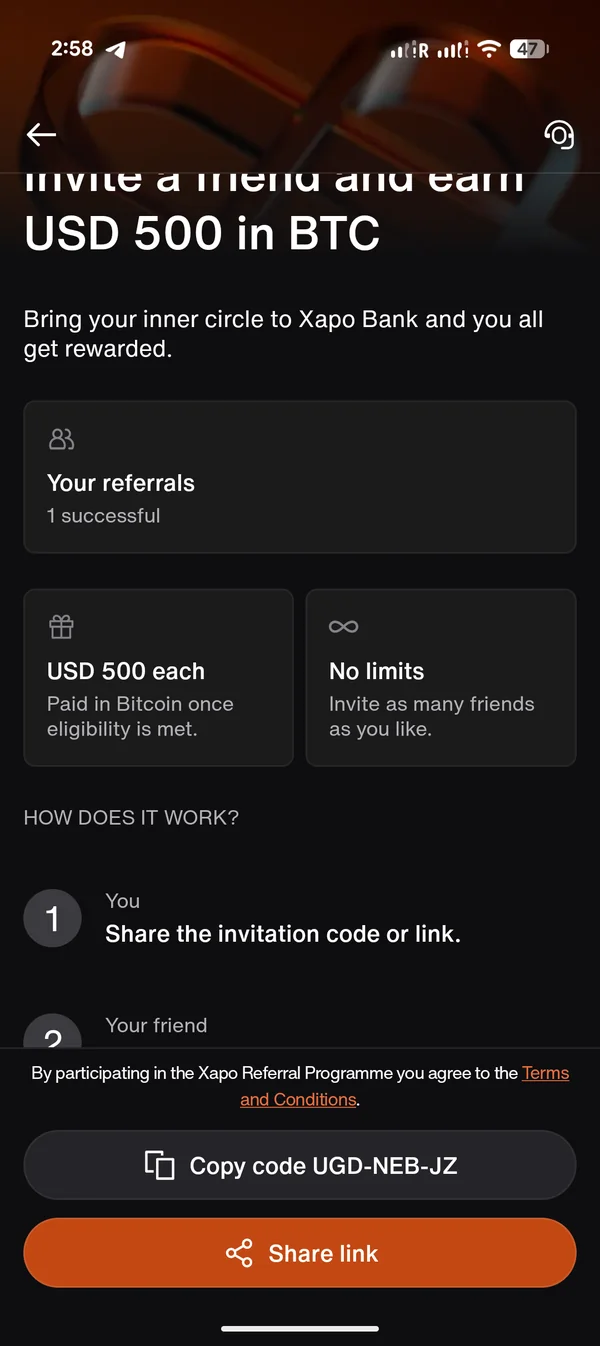

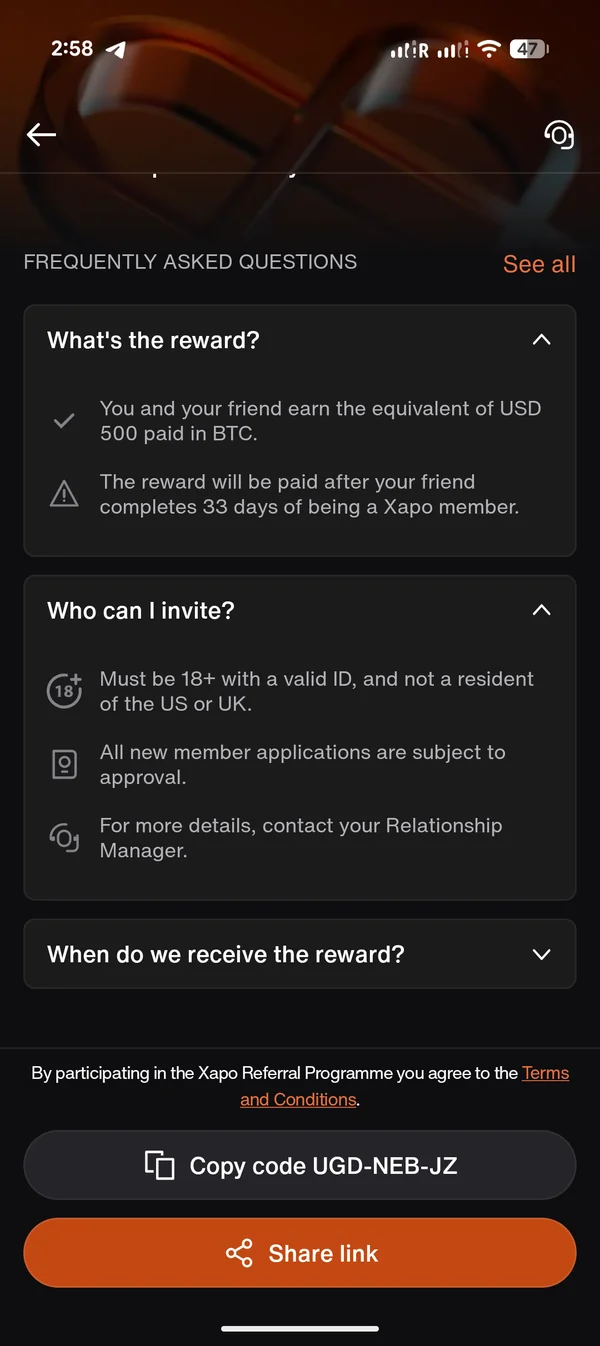

8. The May 2026 referral program is seriously attractive

Xapo simplified the program on May 21, 2026: $500 USD in Bitcoin one-time for both the referrer and the new member, after 33 days of paid membership, no minimum balance. The previous version required $5,000 locked for 33 days — that was the main friction discouraging new sign-ups. The new model makes entry far more accessible. Full details on my referral code page.

What frustrates — the real limitations

1. BTC Credit Fund (2.54% APY) requires a 2 BTC minimum

The most attractive BTC yield tier I mentioned in "What works" — isn't accessible to everyone. You need a minimum of 2 BTC locked to qualify for the 2.54% APY. At ~$75,000 per BTC, that's ~$150,000 in BTC stack — which excludes most users. If your stack is below, you fall back to BTC Savings at 0.5% APY (still fine, but without the boost). An important limitation to know BEFORE building your BTC yield ROI calculation around Xapo.

2. Non-whitelisted crypto deposits can drag

If you deposit USDT or BTC from an external address that isn't yet whitelisted in your Xapo account, the deposit can take longer to credit — Xapo runs an additional verification layer on new addresses (consistent with bank-grade crypto compliance standards). Once the address is whitelisted, subsequent deposits from the same address arrive quickly. Something to plan around if you're doing a first crypto deposit of significant size — do a small test first to validate the whitelist.

3. US and UK restriction = friction for your network

Xapo doesn't accept US or UK residents. It's a regulatory positioning choice (stay within Gibraltar FSC framework without exposing to UK FCA or US FinCEN extraterritoriality), not a red flag — but it means you can't recommend Xapo to a lot of your US/UK contacts. For a non-US/non-UK expat, it's not a problem for personal use, but it limits the referral funnel.

The real cost — 2026 math

Here's the objective math on 1 year of using Xapo Bank, with and without referral code:

| Scenario | Without code | With code (May 2026) |

|---|---|---|

| Annual membership | $1,000 | $1,000 |

| Referral bonus (33 days) | – | +$500 USD BTC |

| USD Savings yield ($10,000 × 3.35%) | +$335/year | +$335/year |

| Net cost year 1 | ~$665 | ~$165 |

| Net cost years 2+ (same usage) | ~$665/year | ~$665/year |

Xapo Bank vs alternatives — honest comparison

| Criterion | Xapo Bank | Wise | Revolut | Coinbase |

|---|---|---|---|---|

| Real licensed bank | ✓ Gibraltar FSC | ✗ E-money | ✗ E-money (mostly) | ✗ Exchange |

| USD account with routing number | ✓ | ✓ | Limited | ✗ |

| Worldwide physical VISA | ✓ | ✓ | ✓ | ✗ |

| Bitcoin under banking license | ✓ | ✗ | Crypto trading (not bank custody) | Exchange custody |

| USD yield | 3.35% APY | 0% | Variable (Stocks) | 0% |

| BTC yield (max tier) | 2.54% APY Credit Fund (min 2 BTC) / 0.5% Savings otherwise | N/A | N/A | Variable (some staking) |

| Integrated Stocks & ETFs | ✓ | ✗ | ✓ (Stocks) | ✗ |

| BTC-collateral loan | ✓ | ✗ | ✗ | ✗ (discontinued) |

| Annual cost | ~$1,000 | Free (transaction fees) | Free/paid plans | Free (spreads) |

| Available non-US/UK | ✓ Designed for it | ✓ | ✓ | Varies by jurisdiction |

Xapo's uniqueness remains: no other institution combines real banking license + USD account + worldwide VISA + native Bitcoin custody into a single product for a non-US/non-UK resident. Sygnum and AMINA Bank in Switzerland have similar positioning but target high-net-worth clients with different account structures and significantly higher minimums. For a regular non-wealthy expat, Xapo remains the most accessible entry point in that category.

Who it makes sense for — and who it doesn't

✅ Xapo Bank makes sense if you tick ≥3 of these

- You're a non-US and non-UK resident (eligibility requirement)

- You receive or hold more than $5,000 USD/year in dollars

- You want a real US routing number without living in the US

- You use (or plan to use) Bitcoin and prefer bank-grade custody over exchange or self-custody

- You travel internationally and need a VISA card that works everywhere without hidden FX fees

- You're willing to pay a premium membership for dedicated financial infrastructure

❌ Xapo Bank doesn't make sense if

- You're a US or UK resident (rejected at signup)

- You want pure self-custody for your Bitcoin (use Coldcard or Ledger)

- You only do occasional international transfers (Wise is free and enough)

- Your annual USD volume is low (<$5,000) — yield doesn't offset membership

- You need a business account for a US LLC (Xapo is personal only — use Wise Business)

My concrete usage after 3 years — LLC + owner draw workflow

The key use case for my profile as an expat with a US LLC: Xapo Bank is my personal destination account for owner draws from my LLC. Here's the concrete workflow many expats with an LLC can replicate:

- My clients (US and European) pay my LLC in USD and EUR via two rails: Wise Business for bank transfers (international IBAN, US routing number, 40+ currencies) and Stripe for online card payments (Stripe payouts land in Wise Business). This is the LLC's main revenue input.

- As a single-member LLC owner, I take owner draws regularly from Wise Business → Xapo Bank personal. USD transfer, no intermediate conversion. Zero FX loss since it stays USD all the way.

- On Xapo Bank (personal account), USD sits at 3.35% APY while idle, and I can spend via the worldwide VISA card while traveling without hidden FX fees.

- Gradual USD → BTC conversion directly in the Xapo app, keeping Xapo custody (not my main BTC stack which is self-custody, but the "liquid" BTC accessible quickly).

The key point: clean separation between LLC business (Wise) and personal (Xapo), USD-native on both sides, zero conversion fees between the two. This is exactly the structure I recommend to clients setting up their LLC with me.

The annual membership (~$1,000) is largely offset by: the 3.35% yield on personal USD balance, the absence of conversion fees on owner draws, active VISA usage while traveling, and the 1-2 referrals I generate per year through my expat community.

FAQ

Is Xapo Bank a real bank or a crypto platform?

A real licensed bank in Gibraltar (GFSC, Permission No. 23171). Not a crypto wrapper. The license is public and verifiable.

How much does Xapo Bank cost per year?

About $1,000/year for the paid membership that unlocks all features. With the May 2026 referral code, year one effectively costs ~$500 after bonus.

How long does account opening take?

Faster than expected for a real licensed bank: a few days for KYC in most cases. Much faster than opening an account at a traditional bank.

Is my Bitcoin safe with Xapo Bank?

100% reserve policy, bank-grade custody in physical bunkers. Safer than most exchanges, less safe than your own hardware wallet. Use for "transactional" / liquid BTC, not your long-term sovereignty stack.

Can I open a Xapo Bank account as a non-US, non-UK resident living abroad?

Yes, fully eligible if you're neither a US nor UK resident. Expats in Panama, Thailand, Georgia, Paraguay, Dubai, EU, etc. are perfectly admissible.

What's the concrete difference vs Wise?

Wise = e-money license, no yield, no Bitcoin, free. Xapo = real licensed bank, 3.35% USD yield, Bitcoin custody, $1,000/year. The two are complementary: Wise for transfers and business, Xapo for storage and Bitcoin under regulation.

How do I claim the $500 referral bonus?

Sign up with a valid code (mine: UGD-NEB-JZ), complete KYC, become a paid member. After 33 consecutive days of active membership, $500 USD in BTC is credited to your wallet. Full details on my referral code page.

Can I cancel my membership easily?

Yes, via in-app support. No pro-rata refund on the prepaid annual membership except in specific cases.